Understanding Medicaid Spend Down: A Guide for Older Adults

Finding healthcare can be difficult for older individuals on fixed incomes. Medicaid, a federal state public insurance program designed to assist those who lack resources in paying for medical treatments, may help those eligible receive coverage, but sometimes income levels exceed eligibility. In such a situation, it could be that a “Medicaid spend down” could be the better solution.

What is a Medicaid Spend Down?

An optional Medicaid Spend-down allows individuals to utilize any income beyond the state Medicaid income limits to meet healthcare costs so as to be eligible for Medicaid coverage. How Does Spending Down Work? Here is how it works:

Example: Imagine that you’re on Medicare, and the state’s Medicaid allowance is $2,000 per month. If your monthly earnings are $2200, you have to spend the $200 extra for healthcare expenses, including your Medicare cost. If you spend $225, Medicaid would cover the additional $50.

| Monthly Income | Medicaid Income Limit | Income Above Limit | Healthcare Expenses | Amount Covered by Medicaid | Explanation |

| $2,200 | $2,000 | $200 | $0 | $0 | No expenses to cover the excess income. |

| $2,200 | $2,000 | $200 | $150 | $0 | Expenses are less than the excess income; no Medicaid coverage. |

| $2,200 | $2,000 | $200 | $200 | $0 | Expenses exactly equal the excess income; no additional Medicaid coverage. |

| $2,200 | $2,000 | $200 | $250 | $50 | Expenses exceed the excess income; Medicaid covers the additional $50. |

| $2,200 | $2,000 | $200 | $300 | $100 | Expenses exceed the excess income; Medicaid covers the additional $100. |

Different Names and Rules

The spend-down down programs may go by various names depending on where you reside, including excess income program, surplus income program, or even medically needy program with states having different durations from one to six months for spending down plans.

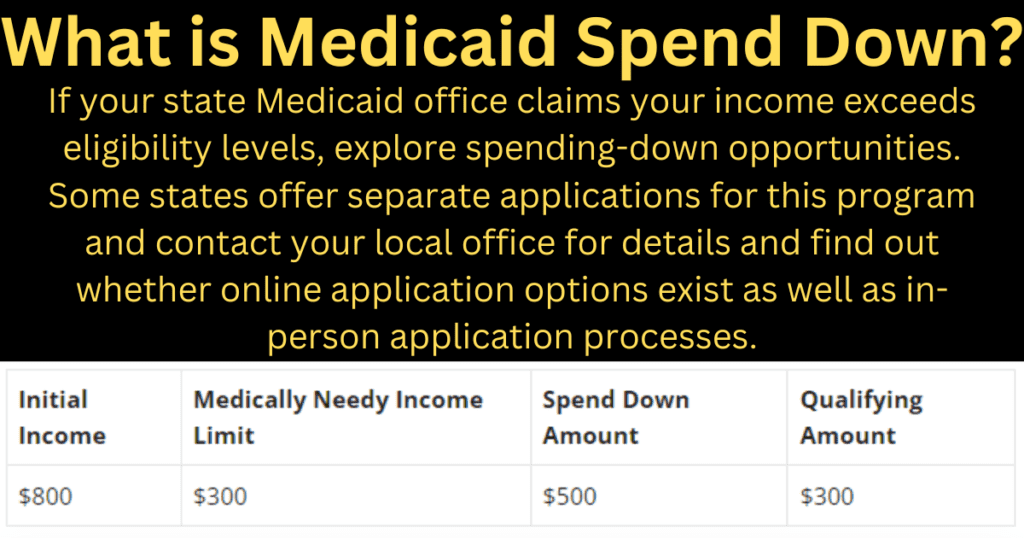

Qualifying for Medicaid Spend Down

Spending down is one of the best ways to qualify for Medicaid when your medical costs exceed its limitations, your assets or income exceed its limitations for long-term medical treatments, or your assets or income surpass Medicaid’s eligibility limitations for long-term treatment. Medically needy programs typically restrict eligibility only to people aged 65+ with disabilities or blindness whose assets or income surpass Medicaid restrictions for such treatment, with spending down being determined by each state’s medically needy income limit, which takes into account your living costs and household size when making eligibility determinations.

Example: If your income is $800 and the medically needy income limit is $300, you would need to spend down $500 to qualify for Medicaid.

| Initial Income | Medically Needy Income Limit | Spend Down Amount | Qualifying Amount |

| $800 | $300 | $500 | $300 |

Applying for a Spend-Down Program

If your state Medicaid office claims your income exceeds eligibility levels, explore spending-down opportunities. Some states offer separate applications for this program and contact your local office for details and find out whether online application options exist as well as in-person application processes.

Qualifying Expenses for Medicaid Spend Down

Here are some health care-related expenses you can spend down your income on:

- Medications

- Paid and unpaid medical bills

- Nursing home care

- Health-related home renovations (e.g., wheelchair ramps)

- Transportation to medical appointments

Keep copies of medical bills and receipts as evidence when showing them to the state Medicaid office during your spend-down period.

Sources of Income to Spend Down

Income includes money that regularly comes your way – for instance from salaries or wages but also from:

- Social Security retirement payments

- Social Security Disability Insurance (SSDI)

- Veterans benefits

- Pensions

- Interest from bank accounts and certificates of deposit

- Dividends from stocks and bonds

States set the income thresholds for Medicaid eligibility, which differ depending on whether you’re single or married. For couples who are married, limits may differ depending on whether either or both spouses require Medicaid.

What Happens if You Don’t Spend Down Enough Income?

If your spend-down period doesn’t allow enough money for savings, Medicaid coverage could temporarily lapse. Reach out to a Medicaid caseworker or the local State Health Insurance Assistance Program (SHIP), as they will assist with any gaps. A Medicaid planner is also helpful when tracking financial matters to avoid penalties imposed by authorities or contacting the local Area Agency on Aging, who can offer budget advice and planning help.

Alternatives if Your State Lacks a Spend-Down Program

If your state doesn’t offer features to allow individuals to spend down, consider enrolling in the Medicaid Buy-In Plan, as it helps working adults under 65 who have disabilities become eligible for Medicaid eligibility. Eligibility requirements vary by state; eligibility rules could include income restrictions or premium payment requirements as well as meeting any other applicable rules; be sure to abide by them even if your income appears inadequate.

Your local area agency on aging can offer free Medicaid planning assistance on available alternatives to medically needy Medicaid. Visit a Benefits Enrollment Center if there’s one near you, or call NCOA’s Helpline for support – simply dial 1800-794-6559! Get started now by giving them a call – call them now on 1-800-794-6559 .

Reference:

| No. | Reference | Link |

| 1 | National Council on Aging. Does Medicare Cover Nursing Homes? What Older Adults and Caregivers Should Know. | https://www.ncoa.org/ |

| 2 | Genworth. 2021 Cost of Care Survey. | https://www.genworth.com/ |

| 3 | KFF. The Medicaid Medically Needy Program: Spending and Enrollment Update. | https://www.kff.org/ |

| 4 | Medicaid.gov. Medicaid Eligibility. | https://www.medicaid.gov/ |

| 5 | U.S. Department of Health and Human Services. Implementation Guide: Medicaid State Plan Eligibility Medically Needy Income Level. | https://www.hhs.gov/ |

| 6 | Centers for Medicare & Medicaid Services. Medicaid Spenddown & Extra Help. | https://www.cms.gov/ |

| 7 | LongTermCare.gov. Medicaid Eligibility. | https://acl.gov/ |

| 8 | KFF. The Medicaid Medically Needy Program: Spending and Enrollment Update. | https://www.kff.org/ |

| 9 | National Council on Aging. Nursing Home Costs and Payment Options. | https://www.ncoa.org/ |

| 10 | Medicare Rights Medicare Interactive. Spend-down program for beneficiaries with incomes over the Medicaid limit. | https://www.medicareinteractive.org/ |

| 11 | Medicaid.gov. Medicaid “Buy-in” Q&A. | https://www.medicaid.gov/ |

Understanding Medicaid Asset Spend-Down Rules:

Navigating Medicaid’s asset spend-down requirements can be confusing due to the varying rules across states and different scenarios based on marital status. Here’s a detailed breakdown to help you understand the key aspects and provide clarity on what you need to do to qualify for Medicaid.

Understanding Medicaid requirements for asset spending may be complex due to different rules in each state and different scenarios depending on marital status, but we’ve put together this comprehensive overview so you can grasp its essential elements and understand how you must proceed if you hope to qualify for Medicaid eligibility.

Understanding Medicaid requirements for asset spending may be complex due to different rules in each state and different scenarios depending on marital status, but we’ve put together this comprehensive overview so you can grasp its essential elements and understand how you must proceed if you hope to qualify for Medicaid eligibility.

Asset Limits for Individuals:

Individuals seeking long-term healthcare through Medicaid typically have an asset limit of around $2,000 in many states. However, there may be exceptions.

| State | Maximum Countable Assets to Qualify for Medicaid |

| Most States | $2,000 |

| Connecticut | $1,600 |

| D.C. | $4,000 |

| Illinois | $17,500 |

| California | No asset limit |

Example: Jane is among those senior citizens living in Illinois who can keep assets worth up to $17,500 while still qualifying for Medicaid benefits, should she move to Connecticut instead, her allowable assets would drop down to just $1600.

Married Couples with Both Spouses Applying for Medicaid:

Most states set an asset limit of $3,000. Couples filing joint Medicaid applications typically consider all assets to be joint property. There may be exceptions, please consult state guidelines.

| State | Asset Limit |

| Arizona | $4000 |

| North Dakota | $6000 |

Example: John and Mary must limit their resources to $6,000 when applying for Medicaid in North Dakota, otherwise the limit in Arizona would be $4,000.

Married Couples with Only One Spouse Applying for Medicaid

If only one spouse qualifies for Medicaid, however, the rules can become more complex. An applicant spouse typically can keep $2,000 of assets while his/her “healthy” partner (i.e. non-applicant partner) will usually have access to an allowance called spousal resource allowance which varies significantly between marriages.

Range: $30,828 to $154,140 (2024 figures)

| State Type | Description | Maximum Retention (2024) | Minimum Retention (2024) | Example |

| 50% States | Healthy spouse retains up to 50% of the couple’s assets, max $154,140. Below $30,828, retains all. | $154,140 | $30,828 | Jack and Susan with $100,000: Susan keeps $50,000, Jack retains $2,000. With $20,000, Susan keeps all $20,000. |

| 100% States | Healthy spouse retains 100% of the couple’s assets, up to $154,140. | $154,140 | N/A | In Florida, Emily and Robert with $150,000: Emily keeps the entire $150,000. |

| 100% Special Rule States | Varying maximum retention amounts for the healthy spouse. | Varies by state | N/A | In South Carolina: $66,480 max. Karen and Tom with $60,000: Karen keeps all $60,000. In Illinois: $129,084 max. |

100% Special Rule States

| State | Maximum Retention (2024) |

| South Carolina | $66,480 |

| Illinois | $129,084 |

100% States Include:

Alaska, Colorado, Florida, Georgia, Hawaii, Illinois, Louisiana, Maine, Minnesota, Mississippi, Nevada, South Carolina, Vermont, Wyoming.

Frequently Asked Questions (FAQ)

What Expenses Qualify for Medicaid Spend Down?

Medicaid Spend down can help those hoping to be approved for Medicaid who do not meet its criteria yet have assets or income above the eligibility threshold. Understanding which assets and income meet this eligibility criterion will enable you to effectively control your finances so as to meet their guidelines and be accepted. The below mentioned qualifying expenses for Medicaid Spend Down.

- Payment covers costs related to doctor visits, hospital stays and medical treatments.

- Cost of medications prescribed by healthcare professionals.

- Hearing aids, wheelchairs and other essential medical devices come at a significant expense.

- Premiums for health insurance coverage such as Medicare Part B and Part D can include monthly premium payments.

- Cost estimates for dental procedures and vision treatments such as glasses and dental procedures.

- Payment arrangements for in-home care services as well as nursing home and assisted living care is now widely accepted and encouraged.

- Travel costs associated with medical and other appointments.

What is Medicaid Spend Down?

Medicaid spend down can be defined as an approach taken to meet the eligibility criteria of the Medicaid program by decreasing income or assets that count against the eligibility thresholds for Medicaid eligibility, typically by spending extra funds or income towards medical costs until one meets the Medicaid threshold requirements.

What is a Spend Down?

Spend down is the practice of reducing an individual’s assets or income in order to meet Medicaid’s eligibility criteria, typically covering medical and related healthcare expenses with excess funds available from savings accounts or liquidating assets that exceed this limit and qualify them for benefits from Medicaid.

What is Exempt from Medicaid Spend Down?

Certain assets and income sources are exempt from Medicaid spend down, meaning they won’t count towards eligibility limits for eligibility purposes. Exemptions differ according to state but typically include:

- Home is where an individual or their partner reside.

- Essential items including clothing, furniture and household products.

- One automobile typically falls outside this exemption category if used solely to transport patients to medical appointments.

- Prepaid burial plans provide peace of mind when planning funeral expenses, by setting aside money in an account dedicated solely for this expense.

- Policies with face values less than $1,500 tend to have lower premium costs and provide adequate protection.

- Property that provides income can be beneficial in providing security to an individual and/or their spouse.

How to Spend Down for Medicaid?

To effectively budget for Medicaid, follow these steps.

- Make an inventory of all sources of income and assets to assess your current financial standing.

- List all medical and healthcare related expenses which could help with spending reduction efforts.

- Set aside funds to cover eligible expenses and keep detailed records and receipts.

- Consult a Medicaid planning expert in order to comply with state-specific regulations and maximize your spend down strategy.

- Provide all required documentation to the local Medicaid office demonstrating how you have spent down your excess income or assets.

Related Post: